Foreign Currency Account in Bangladesh

The Bangladesh Bank has authorized the institutions to maintain multiple types of foreign currency and convertible taka accounts. Bangladesh Bank's rules for opening and maintaining these accounts.

Moreover, persons ordinarily residing in Bangladesh may establish and maintain 'Resident Foreign Currency Deposit (RFCD)' accounts in FC with foreign currency brought in upon their return from international travel. Detailed instructions for opening and administering these accounts are provided below.

Foreign Currency (FC) Accounts are available in the following foreign currencies:

- Dollar (USD),

- British Pound Sterling (GBP),

- Euro, and

- Japanese Yen.

Who can establish an FC account?

- Bangladeshi nationals working or earning abroad, including self-employed Bangladeshi immigrants moving abroad for employment, are permitted to establish an FC Account without an initial deposit.

- Foreign nationals residing abroad or in Bangladesh, as well as foreign firms registered abroad and operating abroad or in Bangladesh.

- Missions abroad and their expatriate personnel.

- Bangladeshi nationals employed by foreign or international organizations operating in Bangladesh, provided their salaries are paid in foreign currency or they receive consultancy fees or honoraria in foreign currency.

- The customs authorities-licensed Diplomatic Bonded Warehouse (duty-free stores).

- Local and Joint Venture contracting firms hired by foreign donors/international donor agencies to execute projects in accordance with the relevant contract, which will be closed as soon as the projects are completed.

- Bangladeshi Shipping Firms and Airline Operators

- Retention quota for merchandise exporters: Exporters providing inputs against back-to-back foreign currency letter of credit.

- EPZ and EZ companies are permitted to establish foreign currency accounts.

- Branch offices, liaison offices, and representative offices may establish FC accounts.

Note: A Private Limited Company operating outside of EZ/EPZ and registered under RJSC cannot establish an FC account.

Conditions, terms, and specifics of numerous FC account types:

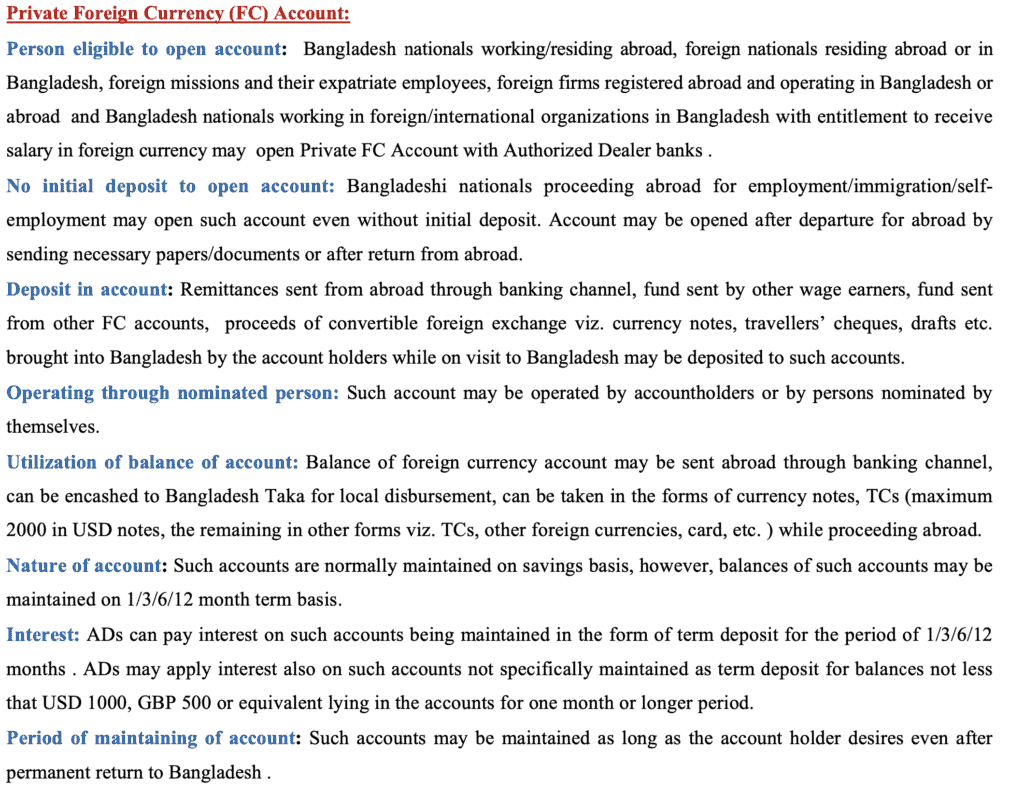

Account in a Private Foreign Currency (FC):

Private FC Accounts can be opened at any of our Authorized Dealer locations.

Bangladeshi citizens living and working abroad;

b. foreign nationals residing in Bangladesh or abroad;

c. diplomatic missions and their expatriate personnel;

d. foreign firms registered overseas and functioning in Bangladesh or internationally;

e. Bangladeshi nationals employed by foreign or international organizations in Bangladesh who are eligible to be paid in foreign currency.

Accounts of the Diplomatic Bonded Warehouse for FC

ADs may establish foreign currency accounts in the names of Diplomatic Bonded Warehouses (duty-free shops) under the following conditions:

a. These accounts may only be credited with convertible foreign currency (notes and coins, travelers' cheques, drafts, cheques or credit card settlements) received on account of the sale of merchandise.

b. Foreign exchange may only be transferred overseas for the import of goods by the bonded warehouse. Foreign exchange may also be transmitted from these accounts to foreign currency accounts maintained with other ADs for the same purpose.

Local and joint venture contracting enterprises' FC accounts

com/one-stop-service-law/">stablish foreign currency accounts in the names of local and joint venture contracting firms hired by foreign donors/international donor agencies to execute projects.a. approved contract with the government authority without Bangladesh Bank's prior consent.

b. Only foreign currency received from donors or donor agencies to cover project expenses may be credited to these accounts.

| Aspect | Details |

|---|---|

| Definition | A Foreign Currency Account (FCA) in Bangladesh is a bank account held in foreign currencies by residents and non-residents for various purposes. |

| Regulatory Authority | The Bangladesh Bank, the central bank of Bangladesh, regulates and oversees FCAs. |

| Types of FCAs | - Non-Resident Foreign Currency Deposit (NFCD) Account - Resident Foreign Currency Deposit (RFCD) Account - Exporter's Retention Quota (ERQ) Account - Importer's Retention Quota (IRQ) Account - Foreign Investor's Taka Account (FITA) - Private Foreign Currency Account (PFCA) and more. |

| Eligibility | - Individuals, including Bangladeshi nationals and non-resident Bangladeshis (NRBs) - Companies, corporations, and foreign investors. |

| Currency Options | FCAs can be maintained in various foreign currencies, such as USD, EUR, GBP, JPY, and more, subject to Bangladesh Bank's approval. |

| Purpose of FCAs | - Facilitating international trade - Remittance of foreign earnings - Investment in Bangladesh - Holding foreign currencies for future use, and more. |

| Documentation | - For individuals: Valid passport, visa, and other KYC documents - For businesses: Incorporation documents, trade licenses, and more, depending on the type of account. |

| Opening Process | - Visit a bank authorized for FCAs with required documents - Fill out an account opening form - Choose the type of FCA - Deposit the required initial amount - Sign an account agreement |

| Operation of FCAs | - FCAs can be operated freely for authorized transactions. - Funds can be transferred abroad and back without significant restrictions. |

| Interest Rates | - The interest rates on FCAs vary and are typically lower compared to local currency accounts. Interest is paid based on the respective foreign currency. |

| Taxation | - Interest income from FCAs is generally tax-exempt in Bangladesh. - Capital gains tax may apply when converting foreign currency back to Bangladeshi Taka. |

FC Accounts of Bangladeshi residents working for foreign/international organizations

Accounts in a foreign currency may be opened:

a. In the names of domiciled Bangladeshi nationals who are employed by foreign or international organizations operating in Bangladesh, if their salaries are paid in foreign currency.

b. This account may only be credited with the foreign currency portion of the salary and debited for all approved current transactions, such as travel expenses, the cost of children's education, medical expenses, etc. These foreign currency accounts also allow for unrestricted local Taka withdrawals.

c. Consultancy fees/honoraria received in foreign currency by the aforementioned category of residents may also be credited to foreign currency accounts, with debits to such accounts subject to the same conditions as stated above.

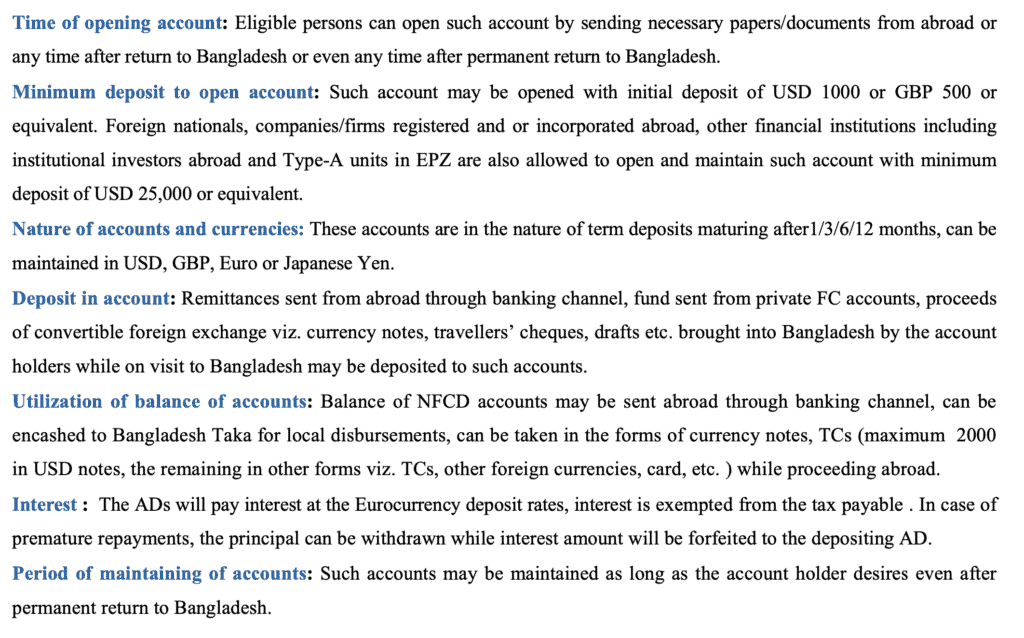

Account for Non-Resident Foreign Currency Deposits (NFCD):

NFCD accounts can be established at our Authorized Dealer locations by:

a. Bangladeshis living and working abroad

b. Bangladeshis with dual citizenship who reside abroad

c. Bangladeshi nationals operating abroad with Bangladeshi diplomatic missions

d. Officers/staff of the government/semi-government organizations/nationalized banks and corporate body employees posted abroad or deputed with international and regional agencies in foreign countries against foreign currency remitted through banking channels or carried in cash.

Account for resident foreign currency deposits (RFCD):

a. Individuals with a permanent residence in Bangladesh may establish an RFCD account with foreign currency brought back from a trip abroad.

b. Residents may establish this account at any time following their return to Bangladesh.

Account for Exporters' Retention Quota (ERQ):

Retention quota accounts may also be established and maintained in the names of deemed exporters for supplying inputs against inland back-to-back foreign currency letter of credit.

ADs are required to strictly adhere to the following:

a. The total amount credited to the direct exporter's retention quota account and foreign exchange paid to the presumed exporter for the supply of inputs cannot exceed the net repatriated amount.

b. FOB export value of the direct exporter; and The foreign exchange shall only be credited to the retention quota account of the deemed exporter upon resolution of the amount against back-to-back LC for deemed export.

Foreign currency accounts for enterprises in the EPZ:

The following procedures will govern the release of foreign currency to enterprises:

Exports originating from EPZs:

a. One hundred percent, eighty percent, and seventy-five percent, respectively, of repatriated export proceeds of Type A, B, and C and industrial unit in EPZ may be retained in FC account in the name of the unit with an AD in Bangladesh.

b. FC account balances may be freely used to satisfy all foreign payment obligations, including import payment obligations of the unit and foreign exchange payment obligations to BEPZA.

Individuals and businesses are able to establish FC accounts in Bangladesh based on their demand and requirements. Other FC accounts include Foreign currency accounts for Initial Public Offerings (IPO); Foreign currency accounts for shipbuilders (exporters); Foreign currency accounts of shipping companies, airlines, and freight forwarders; and Special FC accounts can be opened by obtaining BB's permission and providing evidence.

Bangladesh Bank is the primary regulator of the country's monetary and financial system, as well as the entity in charge of banking and financial legal services in Bangladesh. The Bangladesh Bank Order 1972- President's Order No. 127 of 1972 (Amended in 2003) created it on December 16, 1971. The Governor is also the Chief Executive Officer of this historic institution.

The key tasks of the BB are:

• design and implementation of foreign currency policy;

• holding and managing Bangladesh's official foreign reserves;

• authority for issuing Taka; and

• monitoring banks and other financial institutions.

•BB is governed by a number of laws, rules, and guidelines that help it carry out its responsibilities in regard to the economy's monetary and fiscal systems. Some of these laws are as follows:

· Bangladesh Bank Order 1972;

· Bank Company Act 1991

· Bank Company (Amendment) Act 2013

· Negotiatble Instrument Act 1881

· The Bankers’ Book Evidence Act 1891

· Foreign Exchange Regulations Act 1947

· Foreign Exchange Regulations (Amendment) Act 2015

· Financial Institutions Act 1993

· Financial Reporting Act 2015

· Money Loan Court Act 2003

· Money Laundering Prevention Act,2012

· Money Laundering Prevention (Amendment) Act, 2015

· Anti-terrorism Act, 2009

Mr. Tahmidur Rahman Remura Wahid, a law company in Bangladesh, offers clients confronting legal challenges in banking and finance both litigation and corporate services. Our banking and finance legal services in Bangladesh are provided by a team of experienced lawyers who prepare various documents required to obtain finance, review documents to be submitted to regulatory authorities, provide advice on obtaining finance, and resolve disputes both inside and outside of court using effective dispute resolution skills.

TRW has a significant banking and finance legal services clientele base in Bangladesh, both local and foreign, in the form of banks and other financial institutions, including but not limited to insurance companies, asset management organizations, and so on.

We often represent our clients in money suits, Negotiable Instruments Act 1881 cheque concerns, Money Loan Court Act 2003, Bank Companies Act 1991 mortgage disputes and redemptions, regulatory compliance and communications.

Tahmidur Rahman Remura Wahid, a Dhaka law firm, assists clients in arranging and or structuring loan transactions, project finance, trade finance, construction finance, mergers and acquisitions of corporate entities, resolving transactional disputes, conducting due diligence on mortgaged properties, and so on.

GLOBAL OFFICES:

DHAKA: House 410, ROAD 29, Mohakhali DOHS

DUBAI: Rolex Building, L-12 Sheikh Zayed Road

LONDON: 1156, St Giles Avenue, 330 High Holborn, London, WC1V 7QH

Email Addresses:

info@trfirm.com

info@tahmidur.com

info@tahmidurrahman.com

24/7 Contact Numbers, Even During Holidays:

+8801708000660

+8801847220062

+8801708080817